The UAE does not appear to have an exit tax in any express form for a company that changes its jurisdiction from the UAE to another jurisdiction by way of continuance. The UAE Corporate Tax Law and its implementing decisions do not contain a rule that squarely states either that such an operation is taxable, or that it is expressly exempt or tax-neutral.

That position contrasts with a number of other systems where the legislature has addressed the issue directly, whether in corporate income tax legislation itself or in broader rules dealing with the loss of domestic taxing rights when a company or its assets leave the jurisdiction. Germany, for example, has a general statutory rule in §12 KStG deeming a disposal at fair market value when Germany’s taxing right over the gain from an asset is excluded or restricted, and Portugal’s Article 83 CIRC expressly taxes the difference between market value and tax value when residence is transferred out of Portugal.

That, however, is not the end of the UAE tax story. The real legal question is whether the general rules of UAE Corporate Tax are broad enough to produce, by ordinary operation, consequences that other jurisdictions prescribe expressly as part of “exit taxation”. This requires a two-stage inquiry:

First, the legal nature of redomiciliation itself must be identified.

The next step is to determine whether the ordinary UAE Corporate Tax concepts of transfer, realization, or restructuring are sufficiently broad to capture that event, even though the UAE legislature did not expressly frame it as a case of exit taxation.

The institute of redomiciliation: continuation without termination

Redomiciliation, in its orthodox company-law sense, is not the same as incorporating a new company in another jurisdiction, transferring all assets and liabilities to it, and then liquidating or striking off the old company. In a true continuance, the legal design is that the same body corporate remains in existence while its governing law and register change.

That is why continuance statutes ordinarily preserve the company’s property, rights, obligations, liabilities, and pending proceedings, and deny that a new legal entity has been created. For example,

Mauritius states this with particular clarity: registration by continuation “shall not” create a new legal entity, shall not prejudice the identity or continuity of the body corporate, and shall not affect its property, rights, obligations, or proceedings.

Seychelles says the same in substance, preserving continuity of the company as a legal entity and continuity of its assets, rights, obligations, liabilities, and proceedings.

Hong Kong’s new inward re-domiciliation regime likewise presents itself as preserving legal identity and business continuity, while treating the company as incorporated in Hong Kong from the re-domiciliation date.

The same continuity logic appears on the UAE side:

Article 15 bis of the new Commercial Company Law considers a “transfer of … registration in the Commercial Register from one Competent Authority to another”, emphasizing that the transferred company is “retaining its legal personality”.

ADGM provides that when the company is continued under the law of the other jurisdiction, it thereupon ceases to be an ADGM company and the Registrar records that cessation on that date.

DIFC allows transfer of incorporation abroad only if the destination law provides that the company will continue to have the same property, rights and privileges, remain subject to the same liabilities and debts, and remain party to pending proceedings.

RAK ICC requires satisfactory evidence that, upon continuation abroad, the company will continue to own and enjoy its property and rights and remain liable for its claims, debts, liabilities, and obligations.

In all these regimes, continuance is framed as a continuity-of-personality event, not a transfer of patrimony from one person to another.

This distinction matters for tax analysis because it identifies the factual and legal features that deserve scrutiny in any future investigation. A true continuance ordinarily involves:

no extinction of the old company followed by birth of a new one,

no asset-by-asset conveyance,

no automatic novation of contracts, and

no interruption of pending proceedings.

By contrast, a migration implemented through incorporation of a fresh foreign company, transfer of business and assets to it, and subsequent liquidation of the UAE company plainly presents two different persons and a conventional transfer pattern.

The present inquiry concerns the first category, not the second.

The UAE has not squarely addressed continuance out as an exit-tax event.

The UAE Corporate Tax Law contains detailed rules on taxable persons, tax base, intra-group transfers, and business restructuring relief, but there is no provision specifically addressing the case where an existing UAE company simply continues into another jurisdiction and, as a result, leaves the UAE register.

Articles 26 and 27 deal with qualifying group relief and business restructuring relief. They are not drafted as general corporate emigration provisions. Article 26(4) expressly contains a claw-back rule that can convert an earlier tax neutral intra-group transfer into a market-value transfer if the statutory conditions later fail, and Article 27 gives no gain and loss treatment to defined restructuring transactions. But neither provision says that a pure continuance out of the UAE is itself a deemed disposal at market value.

That silence becomes more significant when placed against comparative law. Other jurisdictions commonly legislate the point:

Germany does so through a general corporate de-taxation rule, and

Portugal expressly does so for transfer of residence.

The UAE, by contrast, has not enacted an equivalent rule targeted at loss of taxing rights through corporate continuance. That legislative omission does not preclude a wider reading of general UAE rules, but it means that any argument for taxability must be built by interpretation rather than by direct application of an explicit exit-tax norm.

The UAE tax concept of “transfer” is broad

The strongest argument for possible taxability under general UAE law comes not from any exit-tax article, but from the UAE’s own treatment of restructuring transactions:

Article 27(1)(a) provides the no gain or loss treatment where a taxable person transfers its entire business or an independent part of it to another person who is a taxable person or “will become a Taxable Personas a result of the transfer in exchange for shares or other ownership interests of the Taxable Person that is the transferee”.

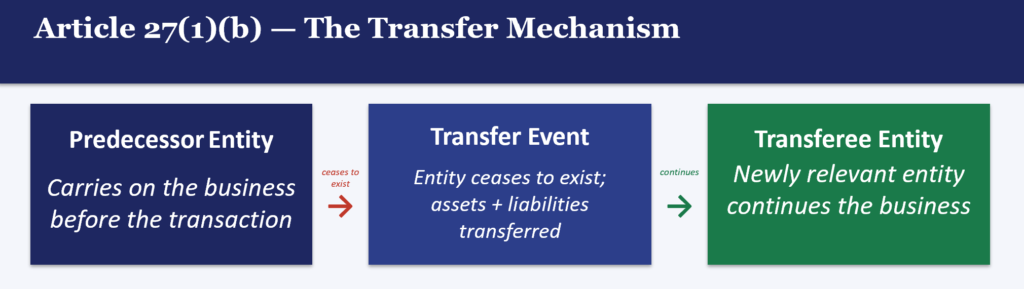

Article 27(1)(b) extends the relief to the cases where “one or more Taxable Persons transfer their entire Business to another Personwho … will become a Taxable Person as a result of the transfer in exchange for shares or other ownership interests of … the transferee, and … the transferor cease to exist as a result of the transfer”.

The text therefore makes clear that UAE tax law does not require both transferor and transferee to have existed as Taxable Persons at the same moment before the transaction. The transferee may become taxable because of the transfer, and the transferor may disappear because of it.

This is particularly evident in the case contemplated by Article 27(1)(b) where:

one entity ceases to exist, while a new or newly relevant entity continues the business, and

the shares or ownership interests in the ceased entity are replaced with shares in the transferee in the hands of the same owners.

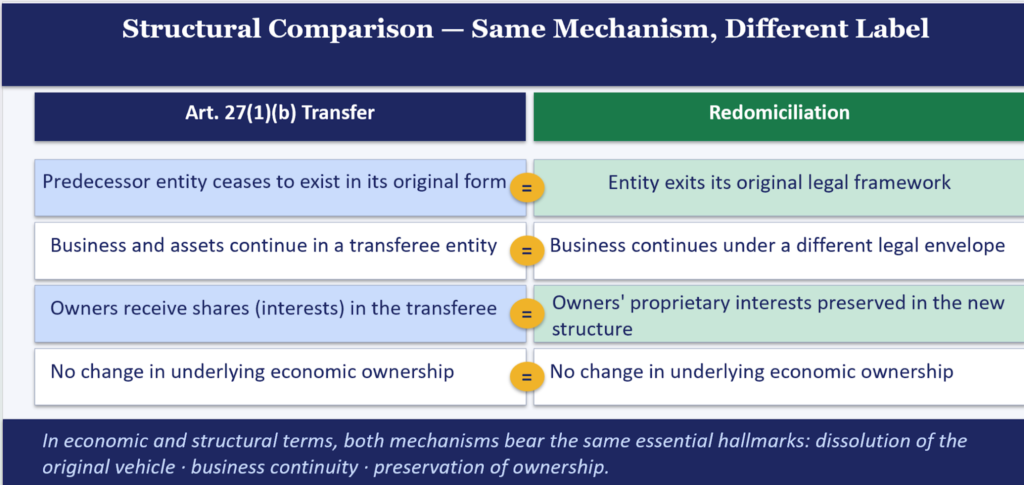

In economic and structural terms, that mechanism bears a great degree of resemblance to redomiciliation. In both cases, the predecessor entity does not continue in its original legal framework, while the business is carried on within a different legal envelope and the proprietorial interests of the owners are preserved through the new structure.

Figure 1 below illustrates a transfer by universal title under Article 27(1)(b), i.e. transfer, which would ordinarily be taxable unless the conditions for BRR are satisfied:

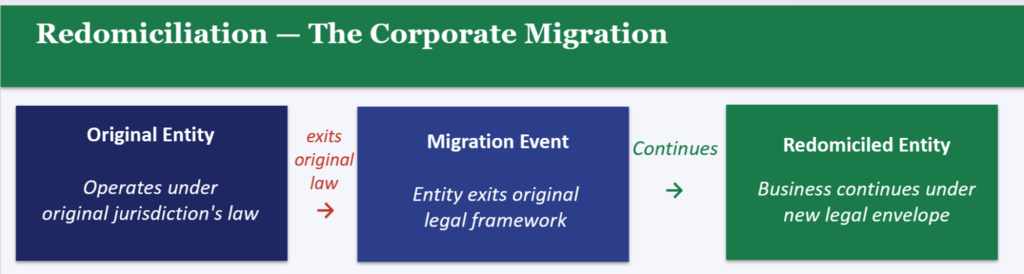

Figure 2 illustrates the typical mechanics of redomiciliation:

And table below sets out a structural comparison between redomiciliation and a restructuring transfer that is taxable in the absence of relief:

That similarity should not be overstated, though. Article 27(1)(b) still operates through the paradigm of a transfer to another Person, with the business moving from a transferor that ceases to exist to a transferee that receives the business and issues equity to the former owners. A pure redomiciliation, by contrast, is normally presented by company law as involving no successor recipient at all, but rather the continuation of the same legal person under a new governing law.

Nevertheless, Article 27(1)(b) materially weakens any narrow argument that a taxable transfer cannot exist unless both entities were already in existence before the transaction or unless the transfer takes the form of an ordinary bilateral conveyance. The provision shows that, for UAE Corporate Tax purposes, transfer may be recognized in a broader restructuring sense, including in circumstances where the predecessor disappears as part of the same legal operation through which the successor framework comes into being.

CTGBRR1 and transfer by operation of law

The FTA’s BRR Guide No. CTGBRR1 reinforces that understanding. Section 3 explains that, “the Corporate Tax Law eliminates the Corporate Tax impact of certain transactions undertaken as part of the restructuring or reorganisation of a Business. Ordinarily, Business restructuring transactions such as mergers or demergers could result in a taxable gain or loss, even where the ultimate ownership of the Business or Taxable Person does not change, or the original owners of the Business or Taxable Person retain an ownership in the restructured Business. In order not to hamper restructuring transactions undertaken for valid commercial or other non-fiscal reasons, the Business Restructuring Relief in Article 27 of the Corporate Tax Law allows certain types of restructuring transactions to take place in a tax neutral manner”.

The Guide also states that, where Article 27 applies, the transferee is seen to continue the business and business activities of the transferor, including continuity of ownership of the assets and liabilities of the business. The Guide gives concrete examples of this approach:

“a legal demerger where the Transferor transfers an independent part of its Business under universal title to another Taxable Person (i.e. the Transferee) in consideration for shares of the Transferee. The Transferor continues to exist after the demerger”.;

“a legal merger where the Transferor transfers its entire Business to the Transferee under universal title, after which … the Transferor is dissolved, or ceases to exist under law, without going into liquidation, and the shares or ownership interests of the Transferor are cancelled by law, and … the owner(s) of the Transferor become the owner(s) of the Transferee, for example, the Transferee issues new shares to the owner(s) of the Transferor in exchange for the transfer”;

“A full legal demerger where the Transferor transfers its entire Business under universal title to at least two or more persons, after which the Transferor entity is dissolved without going into liquidation, and shares of the Transferor entity are cancelled by law. Shareholders of the Transferor entity become shareholders of the Transferee entity”.

Section 5.4 further explains, the consequences of not meeting requirements of Business Restructuring Relief: “Article 27(1) of the Corporate Tax Law does not apply to all transfers of a Business between two Taxable Persons. If the conditions for a no gain or loss transfer are not met …, the transfer would be outside the scope of Article 27… If such a transfer is between Related Parties, the transfer is a transaction that should meet the arm’s length standard… This means the gain or loss resulting from the transfer should be determined based on the arm’s length value of the assets or liabilities being transferred as part of the Business being transferred”.

These passages are important because they show that UAE Corporate Tax can treat movements of business and assets by operation of law in reorganizations as “transfers” in principle, unless a specific relief blocks immediate recognition. This undermines any overly formal taxpayer argument that transfer exists only where there is a classic bilateral conveyance between two pre-existing companies. UAE CT is willing to recognize transfer in a broader, restructuring sense.

Universal title as a tax-significant mode of transfer under UAE law

The Guide’s references to transfer under universal title are especially important. They show that, for UAE Corporate Tax purposes, a “transfer” is not confined to a bilateral conveyance executed asset by asset. The Guide treats juridical movement of a business effected by operation of law as capable of constituting a transfer in principle.

The Guide is therefore best read as accepting that a transfer may occur even where the transferor disappears through the same legal act by which the relevant successor framework comes into being. This is consistent with Article 27 itself. The statutory structure rejects any narrow argument that a transfer requires both transferor and transferee to have existed as taxable persons at the same moment before the transaction. In that respect, UAE Corporate Tax already operates with a concept of transfer that is substantially broader than ordinary bilateral conveyancing.

The law is therefore capable of looking through private-law mechanics and treating universal-succession type movements as transfers for tax purposes. That is the doctrinal foundation on which an aggressive FTA position might rest.

The civil-law notion of universal succession helps explain why this drafting is coherent. The new Civil Transactions Law preserves the classical distinction between the universal successor and the particular successor, but, true to civil-law technique, does so without defining the attributes of universal succession exhaustively.

Article 225 provides that, subject to the rules on inheritance, the effects of a contract extend to the contracting parties and their “universal successors”, unless the contract, the nature of the transaction, or a legal provision indicates otherwise. Article 226 immediately contrasts the particular successor: if a contract creates personal obligations and rights relating to a thing that is subsequently transferred to a particular successor, those obligations and rights pass only if they are essential requirements of the thing and the particular successor had knowledge of them at the time of transfer. The code therefore assumes a deeper and more comprehensive continuity in the case of the universal successor than in the case of the particular successor.

The same dichotomy appears elsewhere in the code. Article 343, dealing with simulation, provides that the real contract is effective between the parties and their universal successors, while creditors and particular successors acting in good faith may rely on the ostensible contract. Article 1055(2) provides that the management and use regime adopted for commonly owned property binds all co-owners and their successors, whether general or particular successors. Article 1204 states that possession transfers to the general successor with its characteristics.

These provisions are revealing in two respects.

they confirm that UAE law still works with the familiar civil-law categories of universal (general) successor and particular successor;

they show that the legislature continues to treat universal succession as a category whose content is assumed rather than spelled out.

The law uses the concept, but leaves its attributes to be reconstructed through doctrine, comparative civilian understanding, and the structure of the code itself.

The discussion above is sufficient to establish that “universal title” in CTGBRR1 is not a casual synonym for transfer, but a reference to a succession-based mode of juridical transmission known to UAE law, distinct from singular transfer to a particular successor.

At the same time, the universal-title material also reveals the limit of the analogy. In the restructuring examples addressed by CTGBRR1, universal succession still operates through a framework of transferor and transferee. Even if the predecessor disappears as part of the same legal operation, the business is described as passing to another person, and the former owners’ interests are replaced by shares or ownership interests in that transferee. That mechanism is structurally close to a merger or demerger. It is not necessarily the same as a pure redomiciliation, where the corporate-law claim is that there is no successor recipient at all and that the same legal person simply continues under a new governing law.

The universal-title analysis therefore strengthens the FTA’s side only to a certain extent. It shows that Corporate Tax is not trapped by conveyancing formalism and that operation-of-law transfers may be taxable in principle.

But it does not by itself prove that every continuance out of the UAE is a transfer to another person. The decisive question remains whether the relevant redomiciliation route is, in law and substance, better characterized as succession to another person or as same-person continuation.

Conversion as a continuity-based restructuring technique

The foregoing civil-law analysis explains why the Guide’s references to transfer under “universal title” are coherent within UAE legal method. It is, however, useful at this point to move from the Civil Transactions Law to the Commercial Companies Law. The latter recognises a restructuring technique that is even closer to redomiciliation than merger or demerger, namely conversion.

Conversion is important because it demonstrates that a company may undergo a profound legal transformation, including re-registration under a new legal form, without being treated as a newly created juridical person and without interruption to its rights and obligations.

This point is reinforced by the FTA’s own treatment of Business Restructuring Relief. Section 3.2 of CTGBRR1, which sets out examples of transactions covered by Article 27(1)(a), expressly includes a case where “a natural person converts their sole proprietorship Business into an incorporated entity” and that natural person holds the shares or interests of the incorporated entity. The same approach appears in Example 4, where Mr A converts his sole proprietorship business into Company A incorporated in the UAE and holds all the shares in Company A. The Guide therefore treats conversion not as something outside the transfer concept, but as a restructuring transaction capable of falling within BRR where the statutory conditions are met.

This is analytically significant for two reasons:

it further confirms that a restructuring transaction may be treated as taxable transfer even where the business moves into a new legal envelope created or recognised through the same operation;

it shows that the tax concept of transfer is broad enough to cover a situation in which the business is carried on thereafter through a legally transformed vehicle whose ownership mirrors the prior economic ownership.

In that respect, conversion stands alongside merger and demerger as evidence that Article 27 is concerned with substantive business reorganisation rather than merely with conventional sale-and-purchase mechanics.

At the same time, conversion differs in an important way from the merger and demerger examples addressed earlier. In the merger and demerger examples involving universal title, the Guide still works through a framework of transferor and transferee. Even where the predecessor disappears by operation of law, the transaction is described as one in which the business passes to another Person, and the former owners’ interests are replaced by shares or ownership interests in that transferee.

Conversion, by contrast, is structurally closer to same-person continuity. Under Article 275(1) of the Commercial Companies Law, “any company may be converted from one form to another while retaining its legal personality…”. Article 283(2) provides that, after conversion and re-registration under the new legal form, the company “shall maintain its legal personality and its rights and obligations prior to such conversion”, while Article 284(2) states that the conversion becomes effective from the date of issuing the commercial licence in the new form. Thus, UAE company law expressly recognises a reorganisation in which the legal form changes, the company is re-registered, yet the juridical person remains the same.

This makes conversion the closest domestic analogy to redomiciliation:

When a company converts, it moves from one statutory form to another, and therefore from one set of governing legal rules to another, while preserving legal personality and continuity of rights and obligations.

Redomiciliation presents a similar structural path. The company ceases to be governed by one company law and comes to be governed by another.

The difference, of course, is that domestic conversion occurs within the same sovereign legal order and under an express statutory continuity rule, whereas redomiciliation to another jurisdiction involves a different registrar, a different corporate nationality framework, and a different external legal system. For that reason, conversion does not prove that redomiciliation must be treated identically. But it does show that UAE law is already comfortable with the idea that a company may be re-registered under a new legal regime without ceasing to be the same legal person.

This makes conversion the closest domestic analogy to redomiciliation. When a company converts, it moves from one statutory form to another, and therefore from one set of governing legal rules to another, while preserving legal personality and continuity of rights and obligations. Redomiciliation presents a similar structural path: the company ceases to be governed by one company law and comes to be governed by another.

The difference, of course, is that domestic conversion occurs within the same sovereign legal order and under an express statutory continuity rule, whereas redomiciliation to another jurisdiction involves a different registrar, a different corporate nationality framework, and a different external legal system.

The significance of conversion is therefore not that continuity defeats transfer, but rather the opposite. CTGBRR1 confirms that conversion may still be treated as a taxable transfer where the conditions for relief are not met. At the same time, the Commercial Companies Law shows that conversion preserves legal personality and the company’s pre-existing rights and obligations. The combined effect of these materials is that a continuity event may still be treated as a transfer for UAE Corporate Tax purposes. This materially strengthens the risk that the absence of dissolution or the preservation of legal personality does not by itself prevent tax recognition of a transfer.

However, conversion does not conclusively resolve the redomiciliation case, because the FTA Guide expressly addresses conversion but does not expressly address continuance into another jurisdiction. The remaining issue is therefore whether redomiciliation is sufficiently analogous to conversion or to transfer under universal title for general UAE Corporate Tax rules to reach it in the absence of an express exit-tax provision.

The real unresolved issue

The decisive issue is therefore no longer whether continuity can coexist with transfer. Conversion already shows that it can. The more precise question is whether a cross-border continuance is sufficiently close, in legal structure and economic effect, to the categories that UAE Corporate Tax already treats as transfer in principle: transfer under universal title and conversion as a continuity event that nonetheless falls within BRR where the statutory conditions are met.

From the FTA’s perspective, the argument for taxability would run as follows:

A pure redomiciliation, although presented in company-law terms as same-person continuation, still produces a legally significant migration of the business into a new legal framework;

The company ceases to be governed by one company law and becomes governed by another;

It is entered on a new register;

The applicable corporate form and legal regime change;

In practical and legal terms, the business thereafter continues under a different juridical framework.

UAE tax law, as demonstrated by Article 27 and CTGBRR1, is not confined to sale-and-purchase formalism and can recognize transfer where the movement of business, assets and liabilities occurs by operation of law as part of a reorganization.

On that reasoning, the absence of a bilateral conveyance or the preservation of personality would not be decisive.

The taxpayer’s response, however, remains substantial. The existing UAE materials do not merely show that continuity can coexist with transfer. Tthey also show that the legislature and the FTA distinguish carefully between different legal techniques:

In merger and demerger, the statutes and the Guide operate through a transferor and transferee structure.

In conversion, the Commercial Companies Law expressly provides continuity of legal personality, rights and obligations, while the FTA Guide separately confirms that conversion can fall within Article 27. In the case of pure redomiciliation, by contrast, there is no express UAE tax provision and no FTA guidance stating that such continuance should be treated as a transfer.

The taxpayer can therefore argue that the State has legislated or guided the position where it wished to do so, but has not done so for outbound continuance. That silence is important in a taxing statute.

The concept of universal title also stops short of solving the problem conclusively. It is true that CTGBRR1 uses that concept in a way that supports a broad notion of tax-significant transfer. It is also true that the Civil Transactions Law preserves the distinction between universal/general successor and particular successor. But the UAE legislation does not define universal succession exhaustively, nor does it say that every same-person legal transformation falls within it. Universal title is therefore useful as an interpretive bridge, but not as a complete answer.

The company-law mechanics of the relevant continuance route therefore become critical. If the route genuinely preserves the same juridical person, with continuity of property, rights, liabilities, proceedings and ownership, the taxpayer’s case is stronger. If, by contrast, the implementation of the route requires or in fact produces novations, fresh assignments, relicensing of assets, replacement of legal titleholders, or a break in the identity of the corporate person, the case begins to look less like pure continuance and more like a transfer. The inquiry is therefore route-specific.

In that regard, the distinction between the UAE regimes is not merely procedural but evidentially important.

ADGM outbound continuance

ADGM presents the clearest same-person model. Section 113 of its Companies Regulation provides that when a company is continued as a body corporate under the laws of the other jurisdiction, it thereupon ceases to be a company formed or registered under the ADGM Regulations, and the Registrar records that cessation on that date. The statute thus ties ADGM cessation directly to the foreign continuance date. There is no statutory suggestion that one entity transfers assets to another. Rather, the same company ceases to be ADGM-registered because it has become continued elsewhere.

When ADGM’s outbound rule is paired with Mauritius, Seychelles, or Hong Kong, the continuity picture remains intact:

Mauritius says continuation does not create a new legal entity;

Seychelles says continuation does not affect continuity of the company as a legal entity or its assets and liabilities;

Hong Kong treats the company as incorporated in Hong Kong from the re-domiciliation date and requires later evidence of deregistration in the old place of incorporation, while the Inland Revenue Department describes the regime as preserving legal identity and business continuity.

For an ADGM continuance into any of these destinations, the better characterization is same-person continuity, not transfer to another person.

DIFC outbound continuance: same person, but with procedural lag

DIFC adopts the same substantive continuity premise, but with less elegant timing mechanics. Article 145(2) of its Companies Law requires that the destination law preserve the company’s property, rights, privileges, liabilities, restrictions, debts, and pending proceedings. That is clearly same-person language. Yet Article 145(3) says “a Company ceases to be a Company within the meaning of this Law when the Company is continued as a Foreign Company and when the Foreign Company files with the Registrar a copy of the certificate or instrument of continuation certified by the appropriate official of the foreign jurisdiction”. In other words, DIFC cessation depends not only on foreign continuance but also on a filing-back step in DIFC.

This procedural lag makes the DIFC route somewhat more exposed to a revenue argument based on sequencing. For a period of time, the foreign jurisdiction may already recognize the company, while DIFC may not yet have fully switched off its own registration. The Authority could seek to use this overlap in registration mechanics to argue that the business moved from one registered and existing legal vehicle into another registered and existing legal vehicle.

In that sense, the taxpayer’s position may be weaker than in the ADGM outbound continuance scenario, where cessation is tied more directly to the foreign continuance date. At the same time, the point should not be overstated: the existence of procedural overlap does not by itself displace the continuity language of Article 145(2), nor does it conclusively establish transfer to another Person. It merely gives the Authority a stronger factual platform from which to advance that argument.

RAK ICC outbound continuance: the potential mismatch, but still continuity

RAK ICC Business Companies Regulations contains the most elaborate discontinuance mechanics. Regulation 190(3) states that “a company that continues as a company incorporated under the laws of jurisdiction outside RAK ICC does not cease to be a company incorporated under these Regulations unless … … the company has filed with the Registrar the … notice of continuation … and … the Registrar has issued a certificate of discontinuance of the company…”. Regulation 190(5) also allows the Registrar to rely on a provisional foreign certificate of continuance where the foreign jurisdiction’s process requires that sequencing. The decisive local switch-off event is therefore the RAK ICC certificate of discontinuance, not simply foreign recognition.

Regulation 190(8) sets forth that “if the Registrar is satisfied that the requirements of these Regulations in respect of the continuation of a company under the laws of a foreign jurisdiction have been complied with, the Registrar shall

issue a certificate of discontinuance of the company in the approved form;

strike the name of the company off the Register of Companies with effect from the date of the certificate of discontinuance…”.

In Regulation 190(9)(b), RAK ICC instructs that “a certificate of discontinuance … is prima facie evidence that … the company was discontinued on the date specified in the certificate of discontinuance”.

The Regulations therefore adopt a distinctly local switch-off mechanism: whatever may already have happened in the foreign jurisdiction, RAK ICC treats discontinuance as occurring, for its own legal purposes, on the date stated in its own certificate.

This drafting has two consequences. First, it strengthens the point that RAK ICC does not make cessation depend automatically on foreign recognition alone. Foreign continuance may be a necessary precondition, but it is not yet the full local legal event. Secondly, it means that a mismatch in timing is not merely possible but structurally contemplated by the Regulations themselves. The foreign jurisdiction may, in substance or provisionally, have already accepted the company’s continuance, while RAK ICC still regards the company as incorporated under its Regulations until the certificate of discontinuance is issued and takes effect.

That potential mismatch gives the Authority a more substantial platform for argument than in the ADGM setting. The Authority could contend that, during this interim period, the business is already operating within a foreign legal framework while the predecessor vehicle has not yet been fully switched off in RAK ICC. From that it might try to argue that the transaction is not merely a seamless same-person continuance, but one in which the business has effectively moved from one legally existing framework into another – also already existing. In other words, subsections (8) and (9) make the sequencing problem more concrete, because they positively assign legal significance to the date of the RAK ICC discontinuance certificate.

At the same time, subsections (8) and (9) should not be read in isolation. Their function is primarily to determine when discontinuance takes effect in RAK ICC and how that date is proved. They do not, by themselves, say that the company’s assets, rights and liabilities pass to another person on that date. Nor do they say that the foreign-recognized company and the RAK ICC company are two different juridical persons between whom a transfer occurs. The provisions are therefore evidential and procedural in nature: they establish the formal date on which RAK ICC ceases to recognize the company as one incorporated under its Regulations, but they do not independently characterize the underlying event as a transfer to another Person.

This is reinforced by the wider structure of Regulation 190. The same regulation that makes the certificate of discontinuance decisive also requires satisfactory evidence that, upon continuation under the foreign law, the company will continue to own and enjoy all its property and rights, remain liable for its debts and obligations, and remain subject to its existing claims and proceedings. That wider continuity language cuts against reading subsections (8) and (9) as creating a separate successor entity that receives the business. The better reading is that the Regulations distinguish between two questions:

what is the date on which RAK ICC stops recognizing the company as locally incorporated, and

what is the juridical nature of the continuance itself.

The former is answered by subsections (8) and (9). The latter remains governed by the continuity logic of the regulation as a whole.

Accordingly, subsections (8) and (9) do not displace the continuity premise, but they do make the RAK ICC route more vulnerable to a tax authority argument based on imperfect synchronisation. In the ADGM model, the legislation aligns cessation more closely with foreign continuance itself. In the RAK ICC model, by contrast, the Regulations expressly interpose a further local act (the issuance of the discontinuance certificate) and attach legal effect to its date. That makes it easier for the Authority to argue that the route involves a more visible transition from one legal framework to another, and therefore comes closer to the kind of juridical movement that UAE tax law may be willing to treat as a transfer in principle.

Even so, the stronger conclusion remains a qualified one. Subsections (8) and (9) strengthen the case for tax controversy, not for tax certainty. They make the sequencing issue sharper and the taxpayer’s same-person-continuity narrative less clean than in ADGM. But they still fall short of an express statement that outbound continuance from RAK ICC constitutes a transfer of business or assets to another Person for UAE tax purposes. Thus, as with DIFC, the provisions strengthen the Authority’s factual and interpretive position without conclusively resolving the legal characterization of the redomiciliation itself.

Conclusion

The UAE does not have an express exit tax, and it does not expressly address outbound continuance. Nevertheless, the general architecture of UAE Corporate Tax and CTGBRR1 (the recognition of transfer under universal title, and the treatment of conversion) shows that the tax law is capable of treating certain legal transformations as taxable transfers even where company law preserves continuity.

This means that the taxpayer cannot rely solely on the argument that the same legal person continues. But nor does it follow that every continuance out of the UAE is taxable. The decisive question remains whether the specific route is sufficiently analogous to the forms of restructuring already recognized by the tax law to justify characterizing it as a transfer in the absence of an express rule.

Our provisional conclusion is therefore as follows:

A pure redomiciliation from the UAE is not clearly tax neutral, because the general UAE tax rules are broad enough to support an argument for taxability by analogy with restructuring transfers, transfers under universal title, and conversion.

At the same time, it is not clearly taxable either, because neither the Corporate Tax Law nor the FTA’s published guidance expressly states that continuance into another jurisdiction is a taxable transfer or deemed disposal. The result is a zone of genuine legal uncertainty.

Within that zone, both sides have serious arguments:

The taxpayer may rely on same-person continuation, continuity of rights and obligations, and the absence of any express corporate emigration rule.

The FTA, by contrast, may rely on the breadth of the UAE concept of transfer, the treatment of operation-of-law restructurings as transfers in principle, and the inclusion of continuity-based conversion within the BRR framework.

The balance between these competing positions will depend heavily on the precise mechanics of the route used and on how closely the facts resemble a true continuance, as opposed to a succession into another legal framework.

Accordingly, it is not safe to proceed on the assumption that redomiciliation is either taxable or non-taxable as a matter of certainty. The issue must instead be analyzed in layers:

first, at the level of company-law characterization, by asking whether the event is properly understood as same-person continuation or as succession into another legal vehicle;

secondly, at the level of tax-law characterization, by asking whether the general UAE concept of transfer, as reflected in Article 27 and CTGBRR1, is broad enough to capture that event;

thirdly, at the level of route-specific implementation, by examining whether the actual mechanics preserve continuity cleanly or instead reveal substitution, re-vesting, re-allocation of legal title, or other features more consistent with a transfer.

Only after all three layers are considered can a defensible conclusion be reached in a given case.

The analysis above is necessarily not exhaustive. It identifies the main lines of interpretation presently available under UAE law, but those lines must be developed further in both directions:

On the one hand, the risks of negative interpretation already identified above should always be tested against the detailed facts of the particular case, including the corporate steps actually taken, the registrar mechanics, the treatment of licences, contracts, assets, liabilities, and the precise form of foreign continuance.

On the other hand, the positive arguments in favour of same-person continuation should likewise be grounded in the facts, and particularly, where possible, in cases where the redomiciliation has already occurred and the practical implementation can be analysed rather than assumed.

Where the redomiciliation has not yet occurred, the legal analysis should not remain abstract. The transaction should instead be planned carefully so as:

to absorb the strongest available positive interpretations and, so far as possible,

to obstruct or minimise the Authority’s access to the negative ones.

In practice, that means that legal characterization, registrar sequencing, documentary record, treatment of assets and liabilities, and the continuity narrative should all be aligned before the migration is implemented, rather than defended only afterwards.

Where the level of uncertainty, value exposure, or fact pattern makes it prudent to seek a private clarification, the argumentation outlined above should not be treated as final. It should instead be extended, particularised, and fully developed by reference to the exact route, the exact legal mechanics, and the exact commercial reasons for the migration.

The same is true where a taxpayer wishes to proceed without clarification but on the basis of a carefully documented filing position. In either case, the present analysis is best understood as a framework for further case-specific development rather than as a substitute for it.

Disclaimer

Pursuant to the MoF’s press-release issued on 19 May 2023 “a number of posts circulating on social media and other platforms that are issued by private parties, contain inaccurate and unreliable interpretations and analyses of Corporate Tax”.

The Ministry issued a reminder that official sources of information on Federal Taxes in the UAE are the MoF and FTA only. Therefore, analyses that are not based on official publications by the MoF and FTA, or have not been commissioned by them, are unreliable and may contain misleading interpretations of the law. See the full press release here.

You should factor this in when dealing with this article as well. It is not commissioned by the MoF or FTA. The interpretation, conclusions, proposals, surmises, guesswork, etc., it comprises have the status of the author’s opinion only. Furthermore, it is not legal or tax advice. Like any human job, it may contain inaccuracies and mistakes that I have tried my best to avoid. If you find any inaccuracies or errors, please let me know so that I can make corrections.